Content

JC1 Macroeconomics

- Article - Another interest rate cut in China? Not necessarily.

- Article - 2014: THE YEAR MONETARY STIMULUS PROVED ITS WORTH

- Video - Interest rate rise: The Winners & The Losers

- Video - Youth Unemployment, Aging population hindering South Korea economic growth

JC2 Market Failure

- Video & Article - Why Education in Singapore works

- Video & Article - Problem Gambling: 60% more cases seen in last 3 years

- Article - 4 shifts in Singapore's approach to healthcare, outlined by PM Lee

Another Interest Rate Cut in China? Not Necessarily.

Zhou Xiaochuan, governor of the People’s Bank of China. Bloomberg News

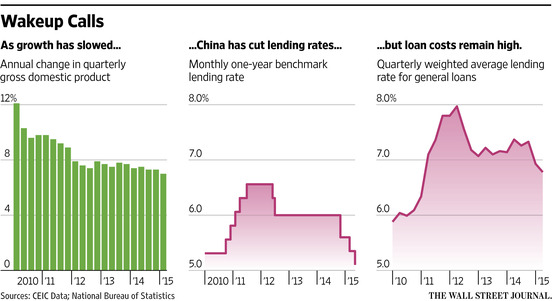

After several rate cuts and moves to release more funds for banks in recent months, China’s central bank might be taking a breather from across-the-board easing measures and instead shift its policy focus to more targeted tools, some economists say.

The People’s Bank of China cut benchmark interest rates in November for the first time in more than two years, triggering a bull run in the domestic stock market. The PBOChas since cut rates two more times — one in March, the other in May — while trimming banks’ reserve requirement ratios twice this year.

There were expectations among market participants recently that another such move may be in the works. Yet the central bank has so far stayed put.

The previous easing measures have helped bring down short-term interest rates but have failed to lower country’s long-term rates, which has been major hindrance to economic growth, economists say.

“It’s not a matter of whether or not the central bank should continue with its easing policies as deflation risks are still rising. It’s more about how to ease,” said Jianguang Shen, an economist of Mizuho Securities.

The People’s Bank of China cut benchmark interest rates in November for the first time in more than two years, triggering a bull run in the domestic stock market. The PBOChas since cut rates two more times — one in March, the other in May — while trimming banks’ reserve requirement ratios twice this year.

There were expectations among market participants recently that another such move may be in the works. Yet the central bank has so far stayed put.

The previous easing measures have helped bring down short-term interest rates but have failed to lower country’s long-term rates, which has been major hindrance to economic growth, economists say.

“It’s not a matter of whether or not the central bank should continue with its easing policies as deflation risks are still rising. It’s more about how to ease,” said Jianguang Shen, an economist of Mizuho Securities.

The seven-day repurchase agreement rate, a benchmark for short-term loans among banks, is at around 2.8%, down from over 4% early this year. The one-year prime lending rate for commercial banks, a guidepost intended to give banks greater say over interest rates, also dropped but only slightly, to 5.05%, from over 5.5%.

China’s banks are still reluctant to lend to businesses for fear of rising bad loans, especially when economic growth slows. Some of the funds released to banks may have gone to the surging stock market. The Shanghai Composite Index has surged 45% so far this year.

“It’s definitely a concern among policy makers that funds are not given to support the real economy,” Mr. Shen said.

The PBOC will likely step up targeted measures to address specific issues in the economy and there may be no more interest rate cuts this year, Haibin Zhu, an economist of J.P. Morgan, said in a recent research note.

Policy options include the Pledged Supplementary Lending, a medium-term liquidity management tool in the banking system, Mr. Zhu said.

The central bank’s view is that economic performance will be better in the second half of the year, meaning there’s less need now for across-the-board easing measures, said Feng Jianlin, an economist of the Beijing Fost Economic Consulting Co., a private think tank.

Researchers with China’s central bank have revised down their forecasts for the country’s economic growth and consumer inflation for 2015, citing increased downward pressure on economic growth. They also expect the growth rate to pick up modestly in the second half of the year as the government steps up efforts to spur expansion, the central bank said in a report published on its website earlier this month.

The government, which last year rolled out easing measures mainly aimed at supporting small firms and the agricultural sector, is now trying to directly lower funding costs for public housing and ensure funds for investment projects by allowing local governments to issue more bonds, Mr. Feng said.

“Boosting investment — that’s the right track to bolster economic growth,” he said.

Growth of fixed-asset investment excluding rural households in China slowed to 11.4% in the first five months of this year, down from an increase of 17.2% in the same period of last year, official data showed. Growth in newly-started projects and funds already in place for existing projects both slowed to multi-year lows.

Not all economists see a halt to China’s rate cut cycle, however.

The government’s recent efforts to cut interest rates and banks’ reserve ratios can help lift investment growth but are not enough to stabilize growth at around 7% — Beijing’s economic growth target for the year — HSBC economists said in a research report released Tuesday.

More-decisive easing measures are needed, they said, adding that they still expect a 50 basis points rate cut and 250 basis point in reserve ratio cuts in the rest of 2015.

–Liyan Qi, Wall Street Journal 25/06/2015

China’s banks are still reluctant to lend to businesses for fear of rising bad loans, especially when economic growth slows. Some of the funds released to banks may have gone to the surging stock market. The Shanghai Composite Index has surged 45% so far this year.

“It’s definitely a concern among policy makers that funds are not given to support the real economy,” Mr. Shen said.

The PBOC will likely step up targeted measures to address specific issues in the economy and there may be no more interest rate cuts this year, Haibin Zhu, an economist of J.P. Morgan, said in a recent research note.

Policy options include the Pledged Supplementary Lending, a medium-term liquidity management tool in the banking system, Mr. Zhu said.

The central bank’s view is that economic performance will be better in the second half of the year, meaning there’s less need now for across-the-board easing measures, said Feng Jianlin, an economist of the Beijing Fost Economic Consulting Co., a private think tank.

Researchers with China’s central bank have revised down their forecasts for the country’s economic growth and consumer inflation for 2015, citing increased downward pressure on economic growth. They also expect the growth rate to pick up modestly in the second half of the year as the government steps up efforts to spur expansion, the central bank said in a report published on its website earlier this month.

The government, which last year rolled out easing measures mainly aimed at supporting small firms and the agricultural sector, is now trying to directly lower funding costs for public housing and ensure funds for investment projects by allowing local governments to issue more bonds, Mr. Feng said.

“Boosting investment — that’s the right track to bolster economic growth,” he said.

Growth of fixed-asset investment excluding rural households in China slowed to 11.4% in the first five months of this year, down from an increase of 17.2% in the same period of last year, official data showed. Growth in newly-started projects and funds already in place for existing projects both slowed to multi-year lows.

Not all economists see a halt to China’s rate cut cycle, however.

The government’s recent efforts to cut interest rates and banks’ reserve ratios can help lift investment growth but are not enough to stabilize growth at around 7% — Beijing’s economic growth target for the year — HSBC economists said in a research report released Tuesday.

More-decisive easing measures are needed, they said, adding that they still expect a 50 basis points rate cut and 250 basis point in reserve ratio cuts in the rest of 2015.

–Liyan Qi, Wall Street Journal 25/06/2015

2014: The year monetary stimulus proved its worth

BY LINDA LIM FOR THE STRAITS TIMES

DEVELOPMENTS in the world economy since the onset of the global financial crisis and ensuing Great Recession in 2008 raised, then answered, many questions about the state of economic policy understanding and efficacy in the world's markets and halls of government.

Initial reactions to the global financial crisis on Wall Street undermined the status quo belief that the United States financial system and its public governance mechanisms were the most advanced in the world, since they had contributed to the highly risky crisis-causing behaviour of financial market actors.

Later, the long-delayed and weak recovery from recession raised doubts about the "Keynes- on-steroids" monetary and fiscal stimulus that the US government pursued. Global concerns were raised about the effectiveness of these policies in the US, and their potentially adverse consequences on the US and world economy.

But the past two years have definitively shown that aggressive monetary stimulus works. This includes the much-maligned quantitative easing (massive bond purchases by central banks) after interest rates reached their "zero lower bound".

The US in particular is enjoying increasingly robust GDP and employment growth, and a rapidly shrinking federal budget deficit. In contrast, Europe's continued fiscal austerity and limited monetary stimulus has proven inadequate to the task of combating deflation, stagnation and persistently high unemployment.

In Japan which has seen two decades of virtual stagnation, Prime Minister Shinzo Abe finally embarked on aggressive monetary easing which showed immediate positive results - until an ill-timed increase in the consumption tax (an attempt to fix its huge budget deficit and world's largest national debt burden) pushed it back into recession.

China recently reversed course by relaxing credit to mitigate a sharp slowdown in GDP growth. This came after two years of monetary tightening to curb its own "unbalanced" growth that had been fuelled by excessive lending by state and private enterprises creating excess capacity in the property market and heavy industry.

Orthodox measures

EACH of these countries/regions, East and West, followed standard orthodox Keynesian counter-cyclical stabilisation policies. This meant stimulating growth with fiscal measures such as cutting taxes and raising government spending and monetary measures such as lowering interest rates and increasing government bond purchases. To fight inflation, this would mean fiscal measures to raise taxes and reduce spending; and monetary measures that raise interest rates and sell government bonds.

The size and timing of these policies may vary. "Too little too late" is blamed for the ineffectiveness of stimulus in the euro zone, while "too much too long" is blamed for China's problems today.

While these are domestic policies, globalisation also has a role to play in their effectiveness and international impact through trade and investment "leakages".

For example, monetary stimulus and the resultant intended inflation caused capital to exit Japan in search of higher returns elsewhere, weakening the yen, which in turn further increased inflation as import prices rose.

Japanese automakers and other manufacturers have since reaped record profits from increased (cheaper) exports, while other companies have been hurt by increased import costs, especially of energy.

The weak yen has also hurt the competitiveness of Korea's - and possibly also China's - exports, while reducing the export stimulus that Europe would otherwise enjoy from the euro's depreciation against the US dollar.

The US dollar's rise is itself fuelled by capital flooding into the US in search of a safe haven amid global political unrest, anticipated higher interest rates already announced by the Fed as its monetary stimulus ceases, and expected higher profits from strengthening US growth.

The strong US dollar dents US exports and increases imports which are now cheaper, but this helps keep inflation (already below target) in check - which in turn keeps Fed tightening at bay, prolonging a bullish stock market.

As for emerging markets, they were whipsawed first in 2010 by capital inflows fleeing recession and monetary stimulus in the crisis-hit advanced economies. This inflow strengthened their currencies, hurt their exports, and fuelled domestic asset bubbles.

Then they were hit in 2013 by a reversal of such flows attracted by anticipated monetary tightening and stronger growth in the US, which caused their currencies to weaken and inflation to rise.

Central banks in these countries resorted in 2014 to raising interest rates, which predictably stabilised currencies and checked inflation, but at the expense of slowing growth. Countries whose commodity exports had fed China's investment-led growth bore the brunt of the slowdown in overall global demand.

The plunge in the price of oil is only the most dramatic expression of this decline in commodity demand, exacerbated by increased supply from US shale (expected) and Libya (unexpected), plus falling demand from Russia as it enters its own recession, and from other commodity exporters themselves.

The fall in oil price is likely to be a net positive to the heavily oil-dependent US economy, strengthening consumer demand and thus imports from the rest of the world, aided by a strong US dollar.

US still the demand driver

WE APPEAR to be back in a 20th-century world where dominant US demand enabled the rapid growth through exports of first Japan, then the "Four Asian Tigers" (South Korea, Taiwan, Hong Kong and Singapore), followed by China, South-east Asia and other emerging markets.

But this development is nothing to be sanguine about.

First, the US today accounts for a much smaller share of world demand than in the 20th century, so its demand alone cannot keep the rest of the world afloat.

Second, the current US recovery aside, the advanced economies of the US, Europe, Japan, Korea, and others will never again enjoy secular growth as high as they did in the last century.

This is due to ageing demographics, mounting budgetary burdens, the normal shift towards consumption of (mostly non-traded) services rather than traded goods at higher income levels, and the spread of social innovations such as a culture of conservation, buy-local movements and the sharing economy.

Third, as their current slowdown suggests, emerging markets may not grow fast enough to absorb the slack, due to both domestic policy and international market constraints. Already there is concern that the slowing growth of world trade may be here to stay, dampening India's and Indonesia's prospects of following a "China model" of export-manufacturing-led growth.

This is unlike the second half of the 20th century when the volume of world trade greatly exceeded that of world GDP, enabling East and South-east Asia's rapid growth.

China itself is gearing up for a "new normal" of slower GDP growth of below 7 per cent (a third less than it experienced over the past three decades). Much of its demand will be internally rather than externally provided, being grounded in home-based services (health, education, eldercare, entertainment) and infrastructure (affordable housing, transportation) rather than imported manufactures and commodities.

For all countries, government macroeconomic stabilisation policy has its limits - with subsequent rounds of monetary and fiscal stimulus being progressively less effective, and easy money having an unpopular side effect in increasing the returns to capital (from cheap borrowing, high profits and booming stock markets) more than to labour, thereby worsening inequality and reducing the boost to mass market consumption that stimulus is supposed to generate.

Policy effectiveness is also hampered by national economic constraints - for example, cheap money and easy credit alone will not encourage businesses to invest in boosting growth if there is excess capacity due to previous poor investment decisions by state- owned enterprises (China), or if labour-market rigidities make it expensive to hire and fire workers (Europe).

Thus most major governments today recognise that ensuring growth in the longer term requires domestic structural reform.

In Japan, it is Mr Abe's "third arrow" of labour market, corporate governance and industrial policy reforms; in Europe, it is labour market liberalisation, budgetary reform and industry deregulation; in the US, it is financial market regulation, entitlement reform, and productivity-enhancing public investments; in China, it is financial market liberalisation, fiscal restructuring and state-owned enterprise reform; in India and Indonesia, it is budgetary reform, industry deregulation, and productivity-enhancing public investments; and so on.

All of these face domestic political and cultural-ideological challenges in being enacted.

Today there is no contestation - if ever there was - between stereotypical "Western" and "Asian" models of economic growth (for example, private versus state capitalism) and political development (for example, authoritarianism versus democracy).

The year 2014 showed us that all governments - from West and East, advanced and emerging economies - respond to macroeconomic imbalances (stagnation, inflation, deflation) with the same set of time-tested and mostly if incompletely effective Keynesian policy tools of monetary and fiscal stimulus or restraint.

All also face serious, if different, political challenges in enacting the domestic structural reforms that they know - and have even announced- are necessary.

We are more alike than we are different, and we are all in the same boat.

2015 will reveal how well we collectively steer it, together.

The writer is professor of strategy at the Stephen M. Ross School of Business, University of Michigan, in the US.

DEVELOPMENTS in the world economy since the onset of the global financial crisis and ensuing Great Recession in 2008 raised, then answered, many questions about the state of economic policy understanding and efficacy in the world's markets and halls of government.

Initial reactions to the global financial crisis on Wall Street undermined the status quo belief that the United States financial system and its public governance mechanisms were the most advanced in the world, since they had contributed to the highly risky crisis-causing behaviour of financial market actors.

Later, the long-delayed and weak recovery from recession raised doubts about the "Keynes- on-steroids" monetary and fiscal stimulus that the US government pursued. Global concerns were raised about the effectiveness of these policies in the US, and their potentially adverse consequences on the US and world economy.

But the past two years have definitively shown that aggressive monetary stimulus works. This includes the much-maligned quantitative easing (massive bond purchases by central banks) after interest rates reached their "zero lower bound".

The US in particular is enjoying increasingly robust GDP and employment growth, and a rapidly shrinking federal budget deficit. In contrast, Europe's continued fiscal austerity and limited monetary stimulus has proven inadequate to the task of combating deflation, stagnation and persistently high unemployment.

In Japan which has seen two decades of virtual stagnation, Prime Minister Shinzo Abe finally embarked on aggressive monetary easing which showed immediate positive results - until an ill-timed increase in the consumption tax (an attempt to fix its huge budget deficit and world's largest national debt burden) pushed it back into recession.

China recently reversed course by relaxing credit to mitigate a sharp slowdown in GDP growth. This came after two years of monetary tightening to curb its own "unbalanced" growth that had been fuelled by excessive lending by state and private enterprises creating excess capacity in the property market and heavy industry.

Orthodox measures

EACH of these countries/regions, East and West, followed standard orthodox Keynesian counter-cyclical stabilisation policies. This meant stimulating growth with fiscal measures such as cutting taxes and raising government spending and monetary measures such as lowering interest rates and increasing government bond purchases. To fight inflation, this would mean fiscal measures to raise taxes and reduce spending; and monetary measures that raise interest rates and sell government bonds.

The size and timing of these policies may vary. "Too little too late" is blamed for the ineffectiveness of stimulus in the euro zone, while "too much too long" is blamed for China's problems today.

While these are domestic policies, globalisation also has a role to play in their effectiveness and international impact through trade and investment "leakages".

For example, monetary stimulus and the resultant intended inflation caused capital to exit Japan in search of higher returns elsewhere, weakening the yen, which in turn further increased inflation as import prices rose.

Japanese automakers and other manufacturers have since reaped record profits from increased (cheaper) exports, while other companies have been hurt by increased import costs, especially of energy.

The weak yen has also hurt the competitiveness of Korea's - and possibly also China's - exports, while reducing the export stimulus that Europe would otherwise enjoy from the euro's depreciation against the US dollar.

The US dollar's rise is itself fuelled by capital flooding into the US in search of a safe haven amid global political unrest, anticipated higher interest rates already announced by the Fed as its monetary stimulus ceases, and expected higher profits from strengthening US growth.

The strong US dollar dents US exports and increases imports which are now cheaper, but this helps keep inflation (already below target) in check - which in turn keeps Fed tightening at bay, prolonging a bullish stock market.

As for emerging markets, they were whipsawed first in 2010 by capital inflows fleeing recession and monetary stimulus in the crisis-hit advanced economies. This inflow strengthened their currencies, hurt their exports, and fuelled domestic asset bubbles.

Then they were hit in 2013 by a reversal of such flows attracted by anticipated monetary tightening and stronger growth in the US, which caused their currencies to weaken and inflation to rise.

Central banks in these countries resorted in 2014 to raising interest rates, which predictably stabilised currencies and checked inflation, but at the expense of slowing growth. Countries whose commodity exports had fed China's investment-led growth bore the brunt of the slowdown in overall global demand.

The plunge in the price of oil is only the most dramatic expression of this decline in commodity demand, exacerbated by increased supply from US shale (expected) and Libya (unexpected), plus falling demand from Russia as it enters its own recession, and from other commodity exporters themselves.

The fall in oil price is likely to be a net positive to the heavily oil-dependent US economy, strengthening consumer demand and thus imports from the rest of the world, aided by a strong US dollar.

US still the demand driver

WE APPEAR to be back in a 20th-century world where dominant US demand enabled the rapid growth through exports of first Japan, then the "Four Asian Tigers" (South Korea, Taiwan, Hong Kong and Singapore), followed by China, South-east Asia and other emerging markets.

But this development is nothing to be sanguine about.

First, the US today accounts for a much smaller share of world demand than in the 20th century, so its demand alone cannot keep the rest of the world afloat.

Second, the current US recovery aside, the advanced economies of the US, Europe, Japan, Korea, and others will never again enjoy secular growth as high as they did in the last century.

This is due to ageing demographics, mounting budgetary burdens, the normal shift towards consumption of (mostly non-traded) services rather than traded goods at higher income levels, and the spread of social innovations such as a culture of conservation, buy-local movements and the sharing economy.

Third, as their current slowdown suggests, emerging markets may not grow fast enough to absorb the slack, due to both domestic policy and international market constraints. Already there is concern that the slowing growth of world trade may be here to stay, dampening India's and Indonesia's prospects of following a "China model" of export-manufacturing-led growth.

This is unlike the second half of the 20th century when the volume of world trade greatly exceeded that of world GDP, enabling East and South-east Asia's rapid growth.

China itself is gearing up for a "new normal" of slower GDP growth of below 7 per cent (a third less than it experienced over the past three decades). Much of its demand will be internally rather than externally provided, being grounded in home-based services (health, education, eldercare, entertainment) and infrastructure (affordable housing, transportation) rather than imported manufactures and commodities.

For all countries, government macroeconomic stabilisation policy has its limits - with subsequent rounds of monetary and fiscal stimulus being progressively less effective, and easy money having an unpopular side effect in increasing the returns to capital (from cheap borrowing, high profits and booming stock markets) more than to labour, thereby worsening inequality and reducing the boost to mass market consumption that stimulus is supposed to generate.

Policy effectiveness is also hampered by national economic constraints - for example, cheap money and easy credit alone will not encourage businesses to invest in boosting growth if there is excess capacity due to previous poor investment decisions by state- owned enterprises (China), or if labour-market rigidities make it expensive to hire and fire workers (Europe).

Thus most major governments today recognise that ensuring growth in the longer term requires domestic structural reform.

In Japan, it is Mr Abe's "third arrow" of labour market, corporate governance and industrial policy reforms; in Europe, it is labour market liberalisation, budgetary reform and industry deregulation; in the US, it is financial market regulation, entitlement reform, and productivity-enhancing public investments; in China, it is financial market liberalisation, fiscal restructuring and state-owned enterprise reform; in India and Indonesia, it is budgetary reform, industry deregulation, and productivity-enhancing public investments; and so on.

All of these face domestic political and cultural-ideological challenges in being enacted.

Today there is no contestation - if ever there was - between stereotypical "Western" and "Asian" models of economic growth (for example, private versus state capitalism) and political development (for example, authoritarianism versus democracy).

The year 2014 showed us that all governments - from West and East, advanced and emerging economies - respond to macroeconomic imbalances (stagnation, inflation, deflation) with the same set of time-tested and mostly if incompletely effective Keynesian policy tools of monetary and fiscal stimulus or restraint.

All also face serious, if different, political challenges in enacting the domestic structural reforms that they know - and have even announced- are necessary.

We are more alike than we are different, and we are all in the same boat.

2015 will reveal how well we collectively steer it, together.

The writer is professor of strategy at the Stephen M. Ross School of Business, University of Michigan, in the US.

Interest Rates Rise: The Winners &The Losers

Youth Unemployment, Aging Population Hindering South Korean Economy.

Market Failure - Merit Goods & Demerit Goods

Why Education In Singapore Works

Problem gambling: 60% more cases seen in last 3 years

The increase is due partly to greater public education efforts, which have raised awareness on problem gambling and encouraged help-seeking behaviour, says Minister for Social and Family Development Tan Chuan-Jin.

SINGAPORE: The Thye Hua Kwan Problem Gambling Recovery Centre and the National Addictions Management Service (NAMS) at the Institute of Mental Health saw 1,000 more cases of problem gambling in the last three years compared to the three-year period prior, Minister for Social and Family Development Tan Chuan-Jin said in Parliament on Tuesday (Jul 14).

Mr Tan said the two key service points for treatment saw a combined total of 2,700 cases between 2012 and 2014 - almost 60 per cent more than the number seen between 2009 and 2011.

“The increase is due partly to greater public education efforts, which have raised awareness on problem gambling and encouraged help-seeking behaviour,” he said.

Responding to questions by MP for Holland-Bukit Timah GRC Christopher de Souza, Mr Tan said that the two institutions are available to help problem gamblers and their families, adding that Thye Hua Kwan treats less serious cases, while NAMS also sees to the more severe pathological gamblers. There are also other private and non-funded community and religious organisations offering similar services, he added.

On the types of counselling used to help gamblers “break out of the vicious cycle”, Mr Tan said the treatment plan for each problem gambler varies depending on the severity of his addiction: “It usually involves a combination of counselling and different types of therapy, conducted on an individual or group basis.

"Psychiatric services may be extended for the more severe pathological gamblers. Financial and legal counselling services, where necessary, are also extended to help the problem gambler and his family cope. Recovering patients are encouraged to join support groups for longer term support.”

While tackling the "complex" issue of problem gambling requires the combined efforts of personal responsibility, family involvement, community involvement and government support, the Minister highlighted that the family is “often in the best position” to detect signs of problem gambling in their loved ones and assist them in seeking treatment.

“Studies have shown that treatment works best if the problem gambler is accompanied by family members,” he said.

Mr Tan also spoke of community support, saying that more Family Service Centres have stepped up efforts to train their counsellors and social workers to provide the first line of counselling and assistance when meeting families faced with problem gambling issues.

Channel NewsAsia 15/07/2015

SINGAPORE: The Thye Hua Kwan Problem Gambling Recovery Centre and the National Addictions Management Service (NAMS) at the Institute of Mental Health saw 1,000 more cases of problem gambling in the last three years compared to the three-year period prior, Minister for Social and Family Development Tan Chuan-Jin said in Parliament on Tuesday (Jul 14).

Mr Tan said the two key service points for treatment saw a combined total of 2,700 cases between 2012 and 2014 - almost 60 per cent more than the number seen between 2009 and 2011.

“The increase is due partly to greater public education efforts, which have raised awareness on problem gambling and encouraged help-seeking behaviour,” he said.

Responding to questions by MP for Holland-Bukit Timah GRC Christopher de Souza, Mr Tan said that the two institutions are available to help problem gamblers and their families, adding that Thye Hua Kwan treats less serious cases, while NAMS also sees to the more severe pathological gamblers. There are also other private and non-funded community and religious organisations offering similar services, he added.

On the types of counselling used to help gamblers “break out of the vicious cycle”, Mr Tan said the treatment plan for each problem gambler varies depending on the severity of his addiction: “It usually involves a combination of counselling and different types of therapy, conducted on an individual or group basis.

"Psychiatric services may be extended for the more severe pathological gamblers. Financial and legal counselling services, where necessary, are also extended to help the problem gambler and his family cope. Recovering patients are encouraged to join support groups for longer term support.”

While tackling the "complex" issue of problem gambling requires the combined efforts of personal responsibility, family involvement, community involvement and government support, the Minister highlighted that the family is “often in the best position” to detect signs of problem gambling in their loved ones and assist them in seeking treatment.

“Studies have shown that treatment works best if the problem gambler is accompanied by family members,” he said.

Mr Tan also spoke of community support, saying that more Family Service Centres have stepped up efforts to train their counsellors and social workers to provide the first line of counselling and assistance when meeting families faced with problem gambling issues.

Channel NewsAsia 15/07/2015

4 shifts in Singapore's approach to healthcare, outlined by PM Lee

SINGAPORE: With changing demographics and disease patterns, Singapore has made four shifts to its approach to delivering good healthcare, Prime Minister Lee Hsien Loong said at the Universal Health Coverage Ministerial Meeting on Tuesday (Feb 10).

"In Singapore, we face the same challenges and difficulties as other societies in delivering good healthcare, because these trade-offs are intrinsic to healthcare delivery. Given these difficulties, we have developed our own approach, and it works reasonably well for us," he told the audience, which included World Health Organization (WHO) Director-General Dr Margaret Chan and Singapore Health Minister Gan Kim Yong.

The Republic's three-pronged approach consists of, first, a focus on public health, such as investing in basic sanitation, compulsory inoculation and mass education; second, a system that "marries the best of a privatised healthcare system with the best aspects of a single-payer model", with Government hospitals restructured to become autonomous, non-profit accounting entities; and third, a balance in healthcare financing between individuals, insurance and Government, with official subsidies supplemented by compulsory savings in the form of Medisave, MediShield and Medifund.

"Insurance premiums will be higher because MediShield Life is a more encompassing scheme, so the government is subsidising the premiums to keep them affordable, especially for the lower-income group," said Mr Lee.

"But because the premiums are going to be higher than before, it is necessary to make MediShield Life compulsory, because with higher premiums there will be more temptation for people to opt out and come back into the healthcare system. And the healthcare system cannot refuse to treat them."

But maintaining good healthcare is an "continuing challenge", said Mr Lee, due to progressions in medical science, an ageing population meaning an increase in the demand for healthcare, and an increase of diseases of affluence rather than poverty, such as more instances of diabetes and obesity.

As a consequence, he said, Singapore has made four shifts to its approach to healthcare:

The Prime Minister said that though the Government is "very mindful" of the risk of excessive healthcare spending, costs were "bound to grow", even over the next five years - a necessary consequence of ensuring affordable healthcare for all.

"We know there will be political pressure to defer necessary fee increases and to manage the services. And it's easy to leave bills to the next generation and focus on the short-term political gain," he said. "If we succumb to this temptation, we will end up with system which becomes non-viable, and will hurt Singaporeans not just financially, but even purely in health terms."

He added that Singapore's healthcare efforts depend on "a supportive political environment", with people willing to take personal responsibility to save for their own healthcare and participate in a universal medical insurance scheme, healthcare providers ensuring that they deliver cost-effective care, and the Government adopting a people-centred approach while staying hard-headed about costs.

"(The Government must) be a trustworthy steward, presenting the trade-offs as they are to the citizens and not sacrifice tomorrow for today’s political gain," said Mr Lee.

"Healthcare is always an emotional and political issue – it's tempting to make promises and say we will do more, we will do better and it will cost less."

He added that every dollar that the Government spends on healthcare is a dollar taken from taxpayers : "This requires an honest conversation among ourselves, and hard choices made, so that we can move ahead together, with clarity on what our society wants and stands for."

The WHO's Director-General Dr Margaret Chan also commented that Singapore's universal health coverage is fair and inclusive, and that it balances the advantages of competition with the need for state intervention.

Channel NewsAsia 10/02/2015

"In Singapore, we face the same challenges and difficulties as other societies in delivering good healthcare, because these trade-offs are intrinsic to healthcare delivery. Given these difficulties, we have developed our own approach, and it works reasonably well for us," he told the audience, which included World Health Organization (WHO) Director-General Dr Margaret Chan and Singapore Health Minister Gan Kim Yong.

The Republic's three-pronged approach consists of, first, a focus on public health, such as investing in basic sanitation, compulsory inoculation and mass education; second, a system that "marries the best of a privatised healthcare system with the best aspects of a single-payer model", with Government hospitals restructured to become autonomous, non-profit accounting entities; and third, a balance in healthcare financing between individuals, insurance and Government, with official subsidies supplemented by compulsory savings in the form of Medisave, MediShield and Medifund.

"Insurance premiums will be higher because MediShield Life is a more encompassing scheme, so the government is subsidising the premiums to keep them affordable, especially for the lower-income group," said Mr Lee.

"But because the premiums are going to be higher than before, it is necessary to make MediShield Life compulsory, because with higher premiums there will be more temptation for people to opt out and come back into the healthcare system. And the healthcare system cannot refuse to treat them."

But maintaining good healthcare is an "continuing challenge", said Mr Lee, due to progressions in medical science, an ageing population meaning an increase in the demand for healthcare, and an increase of diseases of affluence rather than poverty, such as more instances of diabetes and obesity.

As a consequence, he said, Singapore has made four shifts to its approach to healthcare:

- Providing more comprehensive support for outpatient treatment, in the form of the Community Health Assist Scheme to subsidise treatment for lower or middle-class Singaporeans at private GPs

- Replacing MediShield with the universal, compulsory MediShield Life insurance scheme, which will "give better protection from growing bill sizes"

- "Right-siting" services to give people better, more affordable care in their communities, such as by building community hospitals and improving access to GPs and polyclinics

- Encouraging Singaporeans to take better care of their health. This is achieved through campaigns promoting healthier food choices, Active Ageing, and providing more "healthy lifestyle" amenities such as cycling connectors and exercise corners

The Prime Minister said that though the Government is "very mindful" of the risk of excessive healthcare spending, costs were "bound to grow", even over the next five years - a necessary consequence of ensuring affordable healthcare for all.

"We know there will be political pressure to defer necessary fee increases and to manage the services. And it's easy to leave bills to the next generation and focus on the short-term political gain," he said. "If we succumb to this temptation, we will end up with system which becomes non-viable, and will hurt Singaporeans not just financially, but even purely in health terms."

He added that Singapore's healthcare efforts depend on "a supportive political environment", with people willing to take personal responsibility to save for their own healthcare and participate in a universal medical insurance scheme, healthcare providers ensuring that they deliver cost-effective care, and the Government adopting a people-centred approach while staying hard-headed about costs.

"(The Government must) be a trustworthy steward, presenting the trade-offs as they are to the citizens and not sacrifice tomorrow for today’s political gain," said Mr Lee.

"Healthcare is always an emotional and political issue – it's tempting to make promises and say we will do more, we will do better and it will cost less."

He added that every dollar that the Government spends on healthcare is a dollar taken from taxpayers : "This requires an honest conversation among ourselves, and hard choices made, so that we can move ahead together, with clarity on what our society wants and stands for."

The WHO's Director-General Dr Margaret Chan also commented that Singapore's universal health coverage is fair and inclusive, and that it balances the advantages of competition with the need for state intervention.

Channel NewsAsia 10/02/2015