Content

- Video - What is inflation?

- Video - Singapore's labour market, 2014.

- Article - Cutting unemployment, how governments should help those on the dole.

- Video - What is Market Failure?

- Article - Competition watchdog blocks bid by Parkway to buy rival firm.

- Article - Healthcare as a Merit good.

- Article - Markets don't work for healthcare.

What is Inflation?

Singapore's labour market, 2014.

Cutting unemployment

How governments should help those on the dole

ALTHOUGH Britain and America can feel smug about their unemployment rates of 5.6% and 5.3%, other countries are still fire-fighting. The Spanish and Italian governments are grappling with rates of 22.4% and 12.7% respectively, and in June the euro-zone average was 11.1%. But what works when people are not working? A new NBER Working paper* offers a guide for governments desperate to reduce the ranks of the unemployed.

“Active labour market programmes” are schemes meant to help people to find work. They grew out of the American public works programmes of the 1930s, where the government spent billions of dollars busying its citizens with building schools, hospitals and bridges. Today programmes also take the form of training, subsidised private work, or help with finding a job. This sort became widespread in America and Britain in the 1990s, as so-called “welfare-to-work” schemes were expanded. But alongside these programmes, some worry that overly generous welfare benefits make people lazy. They say that threats to cut people's benefits if they do not join such programmes could also boost employment, by prodding people off the sofa and into work.

The authors compare results from hundreds of different studies to find out what works best to boost employment prospects, who it works for, and when. They do what is known as a “meta-analysis,” where they combine statistics from lots of papers to get broader (and more powerful) results. Why look at one policy when you could look at 207?

They split work programmes into two groups. The first group emphasises “work first”, and includes benefit sanctions and helping people with their job searches. The second group includes programmes to invest in training, either off or on the job.

Their results show that in the short-term, the more immediate policies—such as kicking people off benefits—get more impressive results. But the effects quickly fade. In contrast, cuddlier programmes that offer training are disappointing in the short-term, but blossom over time. This fits with other research, which has found that the returns to experience in low-skilled jobs is very low, so there is little benefit from pushing people into the first shelf-stacking job they find. On the other hand, the study implies that building their skills yields long-term rewards.

The authors then compare effects on different groups and find that women and the long-term unemployed are most responsive to the investment programmes, but that young people are slightly less responsive than average. This is slightly worrying for governments in Italy and Spain, where more than two of every five people aged under 25 are unemployed. But they can take some comfort from the paper’s final result. When the authors compared programmes implemented in booms and busts, they found training programmes worked better during recessions when unemployment was high.

Overall, the paper offers some useful lessons. Cutting benefits to “discourage laziness” might save money. But the results suggest that if policymakers really want to tackle unemployment, then they will need to invest in well-targeted training, and risk up-front costs for long-run gains.

* “What works? A Meta Analysis of Recent Active Labor Market Program Evaluations”, by David Card, Jocken Kluve and Andrea Weber. NBER Working Paper No. 21431.

Aug 17th 2015, The Economist

“Active labour market programmes” are schemes meant to help people to find work. They grew out of the American public works programmes of the 1930s, where the government spent billions of dollars busying its citizens with building schools, hospitals and bridges. Today programmes also take the form of training, subsidised private work, or help with finding a job. This sort became widespread in America and Britain in the 1990s, as so-called “welfare-to-work” schemes were expanded. But alongside these programmes, some worry that overly generous welfare benefits make people lazy. They say that threats to cut people's benefits if they do not join such programmes could also boost employment, by prodding people off the sofa and into work.

The authors compare results from hundreds of different studies to find out what works best to boost employment prospects, who it works for, and when. They do what is known as a “meta-analysis,” where they combine statistics from lots of papers to get broader (and more powerful) results. Why look at one policy when you could look at 207?

They split work programmes into two groups. The first group emphasises “work first”, and includes benefit sanctions and helping people with their job searches. The second group includes programmes to invest in training, either off or on the job.

Their results show that in the short-term, the more immediate policies—such as kicking people off benefits—get more impressive results. But the effects quickly fade. In contrast, cuddlier programmes that offer training are disappointing in the short-term, but blossom over time. This fits with other research, which has found that the returns to experience in low-skilled jobs is very low, so there is little benefit from pushing people into the first shelf-stacking job they find. On the other hand, the study implies that building their skills yields long-term rewards.

The authors then compare effects on different groups and find that women and the long-term unemployed are most responsive to the investment programmes, but that young people are slightly less responsive than average. This is slightly worrying for governments in Italy and Spain, where more than two of every five people aged under 25 are unemployed. But they can take some comfort from the paper’s final result. When the authors compared programmes implemented in booms and busts, they found training programmes worked better during recessions when unemployment was high.

Overall, the paper offers some useful lessons. Cutting benefits to “discourage laziness” might save money. But the results suggest that if policymakers really want to tackle unemployment, then they will need to invest in well-targeted training, and risk up-front costs for long-run gains.

* “What works? A Meta Analysis of Recent Active Labor Market Program Evaluations”, by David Card, Jocken Kluve and Andrea Weber. NBER Working Paper No. 21431.

Aug 17th 2015, The Economist

What is Market Failure?

Competition watchdog blocks bid by Parkway to buy rival firm

Concerns that deal will lessen competition and drive prices up

The watchdog against anti-competitive business practice has effectively stopped Parkway Holdings from acquiring outpatient diagnostic chain RadLink- Asia, amid fears that the prices of radiology and imaging services like X-rays and ultrasounds would go up.

In a rare move - likely the first such decision in years - the Competition Commission of Singapore (CCS) yesterday announced its "provisional decision" to block the transaction as it would lead to a "substantial lessening of competition in the affected markets".

Two markets - the provision of radiology and imaging services as well as the supply of radiopharmaceuticals which are essential ingredients in diagnostic processes - were deemed to be likely to see decreased competition.

With less competition, the fear is that prices for radiopharmaceuticals or radiology and imaging services could be driven up.

CCS noted that Parkway and RadLink are each other's closest competitors in providing these services for private outpatients here.

More importantly, it is difficult for new players to break into the sector, while the bargaining power of customers is also weak.

CCS added that the merged entity would have very substantial market share following a merger.

Under its guidelines, the watchdog would have competition concerns if the merged entity has a market share of 40 per cent or more. The radiopharmaceuticals market would also be impacted as Parkway would be the only commercial supplier of radiopharmaceuticals here if the merger is allowed.

No potential new radiopharmaceutical supplier is expected to enter the market in the next two to three years to compete with the merged entity, noted the CCS.

Parkway announced in September that it was acquiring 100 per cent of Singapore-based RadLink for $137 million, but the deal was contingent on it being given the green light by the CCS.

While it is possible for them to appeal, the firms may have already moved on.

Parkway's parent IHH Healthcare stated last Friday that the deal had lapsed, while RadLink's parent company Fortis Healthcare, which is listed in India, announced that it would explore other opportunities.

IHH's Parkway group has 16 radiology facilities here while RadLink has six.

Doctors say that the market for radiology and imaging services is likely a growing one.

"We have an ageing population that requires more of these services. Patients are reading more online and coming into clinics and asking about sophisticated tests," said Dr Chia Shi-Lu, chairman of the Government Parliamentary Committee for Health.

"But not everyone needs the most sophisticated scan, it's up to ethical doctors to recommend the most appropriate one," he cautioned.

Most large public hospitals do their radiology and imaging services in-house.

March 17th 2015, The Straits Times

The watchdog against anti-competitive business practice has effectively stopped Parkway Holdings from acquiring outpatient diagnostic chain RadLink- Asia, amid fears that the prices of radiology and imaging services like X-rays and ultrasounds would go up.

In a rare move - likely the first such decision in years - the Competition Commission of Singapore (CCS) yesterday announced its "provisional decision" to block the transaction as it would lead to a "substantial lessening of competition in the affected markets".

Two markets - the provision of radiology and imaging services as well as the supply of radiopharmaceuticals which are essential ingredients in diagnostic processes - were deemed to be likely to see decreased competition.

With less competition, the fear is that prices for radiopharmaceuticals or radiology and imaging services could be driven up.

CCS noted that Parkway and RadLink are each other's closest competitors in providing these services for private outpatients here.

More importantly, it is difficult for new players to break into the sector, while the bargaining power of customers is also weak.

CCS added that the merged entity would have very substantial market share following a merger.

Under its guidelines, the watchdog would have competition concerns if the merged entity has a market share of 40 per cent or more. The radiopharmaceuticals market would also be impacted as Parkway would be the only commercial supplier of radiopharmaceuticals here if the merger is allowed.

No potential new radiopharmaceutical supplier is expected to enter the market in the next two to three years to compete with the merged entity, noted the CCS.

Parkway announced in September that it was acquiring 100 per cent of Singapore-based RadLink for $137 million, but the deal was contingent on it being given the green light by the CCS.

While it is possible for them to appeal, the firms may have already moved on.

Parkway's parent IHH Healthcare stated last Friday that the deal had lapsed, while RadLink's parent company Fortis Healthcare, which is listed in India, announced that it would explore other opportunities.

IHH's Parkway group has 16 radiology facilities here while RadLink has six.

Doctors say that the market for radiology and imaging services is likely a growing one.

"We have an ageing population that requires more of these services. Patients are reading more online and coming into clinics and asking about sophisticated tests," said Dr Chia Shi-Lu, chairman of the Government Parliamentary Committee for Health.

"But not everyone needs the most sophisticated scan, it's up to ethical doctors to recommend the most appropriate one," he cautioned.

Most large public hospitals do their radiology and imaging services in-house.

March 17th 2015, The Straits Times

Healthcare as a merit good

Healthcare is classified as a merit good because consuming it provides benefits to others as well as to the individual consumer. For example, inoculation against a contagious disease provides protection and clearly generates a private benefit as well as an external one, to those who are protected from catching the disease from those who are inoculated. However, few would want inoculation only to protect others. Therefore, the demand for healthcare will be less than the socially efficient quantity.

Funding healthcare

‘Comprehensive, universal and free, from cradle to grave’ was the stated aim of the NHS when it was established in 1948. However, the cost of healthcare provision has risen to such an extent that many believe it is unsustainable.

The development of new technology, new treatments, and new drugs increases the NHS’s ability to supply, but at the same time encourages demand to such an extent that demand substantially exceeds supply. This creates long waiting lists and shortages of hospital beds. A privatised NHS would allow prices to rise to reflect the true cost of supply. This would, of course, violate the principle of free and universal treatment. However, rising costs have forced a re-think on funding.

NHS is highly labour intensive, employing 1.7 million people. Indeed, only the US department of defense, the Chinese army, Walmart and McDonalds employ more. (Source: BBC) This partly explains the enormous cost of funding the NHS. In 2013/14, spending by the NHS was £109.72b - approximately 20% of all government spending - £2,000 for every person in the UK.

The cost of a night’s stay at a private hospital is around £400, excluding treatment, and a course of treatment could cost up to £300,000.

Extra public money is unlikely to be enough to keep pace with the projected increase in demand for healthcare, which is being driven by an aging populating and rising expectations. In 2005, 17% of the population was over 65 and by 2015 it will rise to 25%.

Funding options

Funding of UK healthcare was the subject of the Wanless Report, named after report chairman, Derek Wanless. The report, which was published in 2002, considered four main options for funding healthcare, in two broad categories:

Publicly funded

The report was particularly critical of private insurance, regarding a system based on private insurance as:

Healthcare and moral hazard

If government intervenes to increase the supply of healthcare, there is a potential government failure in the form of moral hazard.

This means that individuals, knowing that they can get free and effective healthcare, fail to take steps to avoid the risks that the healthcare insures against. For example:

In attempting to resolve the problem of healthcare provision and funding, private insurance has been promoted as an alternative to government funding. However, because a third-party, the insurance provider, bears the cost of any claim, there is an incentive to inflate claims and squander scarce resources.

This is referred to as the problem of third party payment, and in such cases insurance suppliers simply pass on the cost to all policyholders.

Creating internal markets

The NHS is centrally funded and has been so since its formation in 1948. However, given that governments may fail to allocate funds efficiently, and many believe that the NHS should be managed more like a private enterprise.

While most economists accept the inevitability of public funding, in order to reduce inefficiencies, many favour the use of internal markets within the existing state funded structure. These markets are often referred to as quasi markets, and they have become increasing seen as an effective means of allowing the price mechanism some role in healthcare resourcing.

As part of these reforms, hospitals may compete with each other for patients from all over the UK, creating an element of competition that previously did not exist. Patients can exercise their choices, electing to be treated in the hospital of their choice. The most popular hospitals, and presumably the most efficient ones, treat more patients and gain more income from the taxpayer. As with real markets, resources are allocated according to consumer preferences.

In addition, hospitals can contract out elements of their service, such as hospital cleaning, meals and ambulance services.

The problem of free healthcare

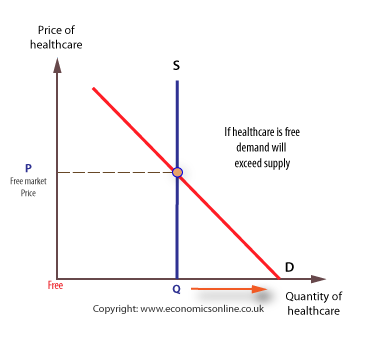

Given that healthcare is a merit good, it is largely provided free at the point of consumption. This means that the price mechanismcannot work to ration scarce resources, as it would for private goods. However, having no price means that there will be a shortage, given that demand will expand to its maximum. This will mean that health resources must be rationed through some other system, such as waiting lists. To understand why a shortage will arise we need to consider the supply of, and demand for, healthcare at different prices.

In the short run the supply of healthcare is fixed, and the supply curve is perfectly inelastic.

The demand for healthcare is at its greatest when it is free to patients, and this means that there is an excess of demand over supply, with waiting lists for treatment and shortages of beds. In this case, waiting lists ration healthcare treatment, rather than charges.

Funding healthcare

‘Comprehensive, universal and free, from cradle to grave’ was the stated aim of the NHS when it was established in 1948. However, the cost of healthcare provision has risen to such an extent that many believe it is unsustainable.

The development of new technology, new treatments, and new drugs increases the NHS’s ability to supply, but at the same time encourages demand to such an extent that demand substantially exceeds supply. This creates long waiting lists and shortages of hospital beds. A privatised NHS would allow prices to rise to reflect the true cost of supply. This would, of course, violate the principle of free and universal treatment. However, rising costs have forced a re-think on funding.

NHS is highly labour intensive, employing 1.7 million people. Indeed, only the US department of defense, the Chinese army, Walmart and McDonalds employ more. (Source: BBC) This partly explains the enormous cost of funding the NHS. In 2013/14, spending by the NHS was £109.72b - approximately 20% of all government spending - £2,000 for every person in the UK.

The cost of a night’s stay at a private hospital is around £400, excluding treatment, and a course of treatment could cost up to £300,000.

Extra public money is unlikely to be enough to keep pace with the projected increase in demand for healthcare, which is being driven by an aging populating and rising expectations. In 2005, 17% of the population was over 65 and by 2015 it will rise to 25%.

Funding options

Funding of UK healthcare was the subject of the Wanless Report, named after report chairman, Derek Wanless. The report, which was published in 2002, considered four main options for funding healthcare, in two broad categories:

Publicly funded

- Taxpayer funded, where healthcare funded by the taxpayer out of general government funds, using tax revenues from all sources, namely the current UK system. Healthcare is provided free to patients, with resource allocation being driven by need, rather than income and the operation of the price mechanism.

- Social insurance, where employees and employers make compulsory contributions towards healthcare and where provision is also free at the point of need. This is often called the European model of healthcare funding.

- Private insurance - where individuals pay premiums (insurance fees) to private companies, and then ‘claim’ when receiving treatment. This approach dominates healthcare funding in the USA, although it is currently under review given the large numbers of American citizens who have no private insurance, or who are significantly under-insured.

- Out-of-pocket payments, where patients pay doctors or hospitals directly for their treatment, such as paying a fee for each visit to the doctor, for each treatment or medicine prescribed.

The report was particularly critical of private insurance, regarding a system based on private insurance as:

- Inequitable - unfair on the less well-off.

- Having high administration costs

- No incentive for cost control - note the problem of third-party payment.

Healthcare and moral hazard

If government intervenes to increase the supply of healthcare, there is a potential government failure in the form of moral hazard.

This means that individuals, knowing that they can get free and effective healthcare, fail to take steps to avoid the risks that the healthcare insures against. For example:

- Over-eating, because people know that there is free treatment for the problems associated with obesity, such as tablets for high blood pressure.

- Smoking, because lung infections can easily be treated with antibiotics.

- Drug abuse, because emergency treatment is freely available.

In attempting to resolve the problem of healthcare provision and funding, private insurance has been promoted as an alternative to government funding. However, because a third-party, the insurance provider, bears the cost of any claim, there is an incentive to inflate claims and squander scarce resources.

This is referred to as the problem of third party payment, and in such cases insurance suppliers simply pass on the cost to all policyholders.

Creating internal markets

The NHS is centrally funded and has been so since its formation in 1948. However, given that governments may fail to allocate funds efficiently, and many believe that the NHS should be managed more like a private enterprise.

While most economists accept the inevitability of public funding, in order to reduce inefficiencies, many favour the use of internal markets within the existing state funded structure. These markets are often referred to as quasi markets, and they have become increasing seen as an effective means of allowing the price mechanism some role in healthcare resourcing.

As part of these reforms, hospitals may compete with each other for patients from all over the UK, creating an element of competition that previously did not exist. Patients can exercise their choices, electing to be treated in the hospital of their choice. The most popular hospitals, and presumably the most efficient ones, treat more patients and gain more income from the taxpayer. As with real markets, resources are allocated according to consumer preferences.

In addition, hospitals can contract out elements of their service, such as hospital cleaning, meals and ambulance services.

The problem of free healthcare

Given that healthcare is a merit good, it is largely provided free at the point of consumption. This means that the price mechanismcannot work to ration scarce resources, as it would for private goods. However, having no price means that there will be a shortage, given that demand will expand to its maximum. This will mean that health resources must be rationed through some other system, such as waiting lists. To understand why a shortage will arise we need to consider the supply of, and demand for, healthcare at different prices.

In the short run the supply of healthcare is fixed, and the supply curve is perfectly inelastic.

The demand for healthcare is at its greatest when it is free to patients, and this means that there is an excess of demand over supply, with waiting lists for treatment and shortages of beds. In this case, waiting lists ration healthcare treatment, rather than charges.

Economics Online

Markets don't work for health care

Commentary: Without a government role, we're sicker and poorer

WASHINGTON (MarketWatch) -- Some of the most strident opposition to health-care reform stems from the literally fatal misconception that markets are the answer to our medical needs.

According to this libertarian view, government intervention in health care is never justified and always harmful.

In fact, totally free markets are abysmally bad at delivering health care. That's why every advanced economy, to one degree or another, has given government a large role in providing health care to its citizens.

We've tried the market approach to health care and the result has always been the same: Poor health and poor people.

Poverty and disease go together, and the causation goes both ways. Show me a country that keeps the government out of health care and I'll show you a country that spends too much on death and not enough on life.

I'm not arguing that everything government does is good, or that everything the private sector does is bad. It's clear that government actions can have their own failures that make health care more expensive or less effective. All I'm arguing here is that relying on markets exclusively leaves us poorer and sicker.

The elegant theory

More than two centuries ago, Adam Smith theorized that markets lead to the best economic outcomes because all parties in a transaction look out for their own interests. It is not the benevolence of the baker that provides our daily bread, but her profit motive.

The elegant theory of the invisible hand often breaks down in practice, however. The theory assumes that both parties are certain of what they want, that they have complete and perfect knowledge of the price and quality of what's being bought and sold, and that the costs and benefits of the transaction remain exclusively with the buyer and the seller.

In the case of health care, those assumptions are fatally flawed. Those who've studied it have found pervasive market failures in health care that lead to inefficient outcomes. Broadly, those market failures can be categorized as uncertainty, adverse selection, moral hazard, asymmetric information, free riding, monopolistic behavior and externalities. The result is lower quality health care and higher costs.

The failures

Health care is fraught with uncertainty. We don't know when or if we'll get sick, or what disease we'll get.

In some cultures, people save vast amounts of money to insure themselves against illness, but such precautionary savings are a drag on the economy. Rather than investing in a new business, or in a child's education, money is put aside to guard against every possible calamity. Too much is saved because of uncertainty.

Group insurance can mitigate the problem of uncertainty. If we all pool our savings, each of us individually won't need to save as much. Some of us may get expensive illnesses, but most of us won't. Yet each of us is covered if the worst happens, and the money we don't have to save as a precaution can be used for other things, from 72-inch plasma TVs to research into a new cancer-fighting drug.

Some people can afford insurance, but don't buy it because they know if something awful happens, they'll survive anyway as wards of the state, or by declaring bankruptcy once medical costs overwhelm them. These people are known as free riders, because they don't pay their way. Half of all bankruptcies are due to medical problems, and we all pay for those bankruptcies through higher interest rates or higher prices.

Insurance creates its own market failures. Unless insurance is mandatory, only those who think they'll actually need the insurance will buy it; healthy people are less likely to buy insurance because it may not pay off for them. That's called adverse selection. Insurance companies guard against adverse selection by trying to require everyone to buy coverage, or by denying benefits to sick people.

The moral hazard

The flip side of adverse selection is moral hazard. If you're insured, health care becomes an all-you-can-eat buffet. Some people consume too much unnecessary care because it's essentially free.

The theory of free markets assumes everyone has complete knowledge of the price and quality of the things they buy or sell, but that's rarely true in health care. Only I know if I was already sick when I bought insurance. Only my doctor knows if the treatment she prescribes will make me better or make her richer.

Insurance companies, doctors, hospitals and drug companies can maximize their profits by exercising monopolistic or monopsonistic powers. Doctors have been able to artificially reduce the supply of medical services. Insurance companies have the market power to squeeze hospitals and doctors.

Drug companies can command exorbitant profits because of patent protections, even as they underinvest in relatively unprofitable drugs that could have a great benefit to society. This explains why we have dozens of almost identical drugs to treat depression, but no vaccine against malaria, one of the world's great killers.

Perhaps the largest market failures in health care come from externalities, which are costs borne by -- or benefits that accrue to -- those outside the transaction.

Healthier, wealthier

Health is not only a benefit to the individual, but to society as a whole. My health makes you better off.

Healthier societies are wealthier, because they take advantage of more of their human potential. Sicker societies underinvest in human capital because early death or chronic illness reduce the payoff from education.

If we relied strictly on market forces to provide health care, we'd be sicker and poorer. As anyone who's lived in a Third World country knows, the market alone can't provide clean water or sewage systems. The market alone can't prevent epidemics.

The dog-eat-dog market alone can't make us healthier, or wealthier. We're better off if we act together. The debate should be over what sort of role government should play, not over whether government is necessary.

August 20th, 2009, Market Watch

WASHINGTON (MarketWatch) -- Some of the most strident opposition to health-care reform stems from the literally fatal misconception that markets are the answer to our medical needs.

According to this libertarian view, government intervention in health care is never justified and always harmful.

In fact, totally free markets are abysmally bad at delivering health care. That's why every advanced economy, to one degree or another, has given government a large role in providing health care to its citizens.

We've tried the market approach to health care and the result has always been the same: Poor health and poor people.

Poverty and disease go together, and the causation goes both ways. Show me a country that keeps the government out of health care and I'll show you a country that spends too much on death and not enough on life.

I'm not arguing that everything government does is good, or that everything the private sector does is bad. It's clear that government actions can have their own failures that make health care more expensive or less effective. All I'm arguing here is that relying on markets exclusively leaves us poorer and sicker.

The elegant theory

More than two centuries ago, Adam Smith theorized that markets lead to the best economic outcomes because all parties in a transaction look out for their own interests. It is not the benevolence of the baker that provides our daily bread, but her profit motive.

The elegant theory of the invisible hand often breaks down in practice, however. The theory assumes that both parties are certain of what they want, that they have complete and perfect knowledge of the price and quality of what's being bought and sold, and that the costs and benefits of the transaction remain exclusively with the buyer and the seller.

In the case of health care, those assumptions are fatally flawed. Those who've studied it have found pervasive market failures in health care that lead to inefficient outcomes. Broadly, those market failures can be categorized as uncertainty, adverse selection, moral hazard, asymmetric information, free riding, monopolistic behavior and externalities. The result is lower quality health care and higher costs.

The failures

Health care is fraught with uncertainty. We don't know when or if we'll get sick, or what disease we'll get.

In some cultures, people save vast amounts of money to insure themselves against illness, but such precautionary savings are a drag on the economy. Rather than investing in a new business, or in a child's education, money is put aside to guard against every possible calamity. Too much is saved because of uncertainty.

Group insurance can mitigate the problem of uncertainty. If we all pool our savings, each of us individually won't need to save as much. Some of us may get expensive illnesses, but most of us won't. Yet each of us is covered if the worst happens, and the money we don't have to save as a precaution can be used for other things, from 72-inch plasma TVs to research into a new cancer-fighting drug.

Some people can afford insurance, but don't buy it because they know if something awful happens, they'll survive anyway as wards of the state, or by declaring bankruptcy once medical costs overwhelm them. These people are known as free riders, because they don't pay their way. Half of all bankruptcies are due to medical problems, and we all pay for those bankruptcies through higher interest rates or higher prices.

Insurance creates its own market failures. Unless insurance is mandatory, only those who think they'll actually need the insurance will buy it; healthy people are less likely to buy insurance because it may not pay off for them. That's called adverse selection. Insurance companies guard against adverse selection by trying to require everyone to buy coverage, or by denying benefits to sick people.

The moral hazard

The flip side of adverse selection is moral hazard. If you're insured, health care becomes an all-you-can-eat buffet. Some people consume too much unnecessary care because it's essentially free.

The theory of free markets assumes everyone has complete knowledge of the price and quality of the things they buy or sell, but that's rarely true in health care. Only I know if I was already sick when I bought insurance. Only my doctor knows if the treatment she prescribes will make me better or make her richer.

Insurance companies, doctors, hospitals and drug companies can maximize their profits by exercising monopolistic or monopsonistic powers. Doctors have been able to artificially reduce the supply of medical services. Insurance companies have the market power to squeeze hospitals and doctors.

Drug companies can command exorbitant profits because of patent protections, even as they underinvest in relatively unprofitable drugs that could have a great benefit to society. This explains why we have dozens of almost identical drugs to treat depression, but no vaccine against malaria, one of the world's great killers.

Perhaps the largest market failures in health care come from externalities, which are costs borne by -- or benefits that accrue to -- those outside the transaction.

Healthier, wealthier

Health is not only a benefit to the individual, but to society as a whole. My health makes you better off.

Healthier societies are wealthier, because they take advantage of more of their human potential. Sicker societies underinvest in human capital because early death or chronic illness reduce the payoff from education.

If we relied strictly on market forces to provide health care, we'd be sicker and poorer. As anyone who's lived in a Third World country knows, the market alone can't provide clean water or sewage systems. The market alone can't prevent epidemics.

The dog-eat-dog market alone can't make us healthier, or wealthier. We're better off if we act together. The debate should be over what sort of role government should play, not over whether government is necessary.

August 20th, 2009, Market Watch