Contents

1. Introduction to Economics

a) What is Economics - Video

b) Opportunity cost and comparative advantage - Video

c) 60 seconds adventure in Economics - Rational Choice Theory - Video

2. Current Affairs

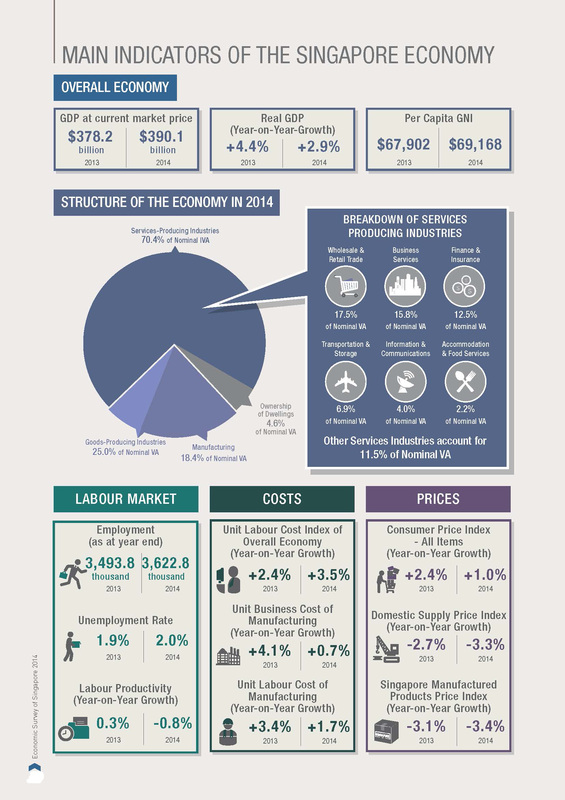

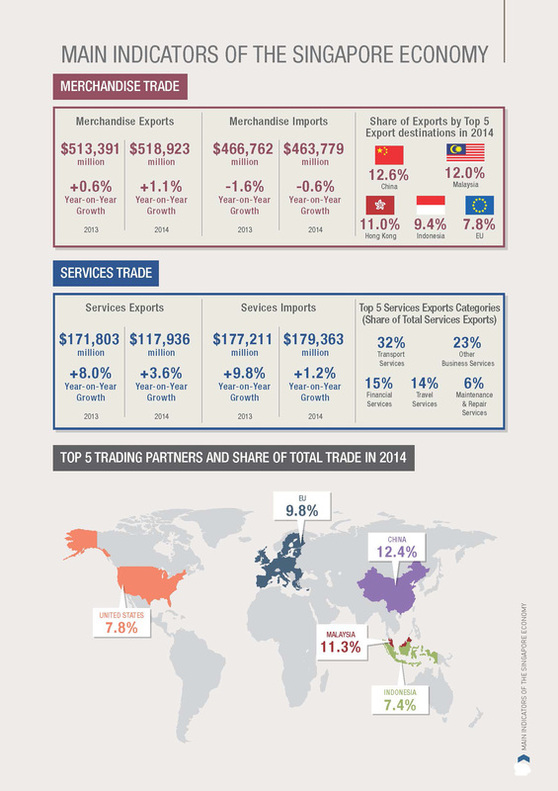

a) Main Indicators of Singapore Economy 2014 - Chart

b) Trade:Child's Play - Video

c) What dark secret is in Singapore's basement? - Article

d) Why the Swiss unpegged the franc - Article

e) Swiss bank's currency u-turn hurts watchmakers, skiers and traders - Article

f) Why are the oil prices falling?- explained in 60 seconds - Video

g) Get used to cheap oil. Why lower prices may stick around. - Article

3. Students' Reflections

a) What is Economics - Video

b) Opportunity cost and comparative advantage - Video

c) 60 seconds adventure in Economics - Rational Choice Theory - Video

2. Current Affairs

a) Main Indicators of Singapore Economy 2014 - Chart

b) Trade:Child's Play - Video

c) What dark secret is in Singapore's basement? - Article

d) Why the Swiss unpegged the franc - Article

e) Swiss bank's currency u-turn hurts watchmakers, skiers and traders - Article

f) Why are the oil prices falling?- explained in 60 seconds - Video

g) Get used to cheap oil. Why lower prices may stick around. - Article

3. Students' Reflections

INTRODUCTION TO ECONOMICS

What is Economics

Opportunity Cost & Comparative Advantage

Rational Choice Theory

CURRENT AFFAIRS

Main Indicators of Singapore Economy2014

Trade: Child's Play

What dark secret is in the S'pore basement?

There are things every society is not proud to be associated with, but which still exist

I had not heard of the child in the basement, the one who is in our midst. Until I read The Ones Who Walk Away From Omelas by American writer Ursula Le Guin, and wished more people would read it. This is the gist of the story: In the city of Omelas, life couldn't be better. The people are happy, they have everything they want and they live life to the fullest.Except for one dark secret that they share.

There is this child who is kept locked in a basement in utter misery, deprived and tortured. The author does not say why this is so, or what the child has done to deserve this terrible imprisonment.Only that it is necessary for the city's continued success and contentment. Free him and everything that made the city such a wonderful place will disappear.

"They all know it is there, all the people of Omelas. Some of them have come to see it, others are content merely to know it is there. They all know that it has to be there. Some of them understand why, and some do not, but they all understand that their happiness, the beauty of their city, the tenderness of their friendships, the health of their children, the wisdom of their scholars, the skill of their makers, even the abundance of their harvest and the kindly weathers of their skies, depend wholly on this child's abominable misery."

Most accept this unwritten social contract that guarantees their happiness.But not everyone is happy with this state of affairs. There are those who cannot stand the injustice and leave the city.

"They leave Omelas, they walk ahead into the darkness, and they do not come back. The place they go towards is a place even less imaginable to most of us than the city of happiness. I cannot describe it at all. It is possible that it does not exist. But they seem to know where they are going, the ones who walk away from Omelas."

As you can see, it is a strange tale but even based on this very short summary, most of us instinctively understand what the story is about and can identify with the troubling issues this allegory raises.

Writing in The New York Times earlier this month, David Brooks offered various interpretations of the story. One is that it's about exploitation - of cheap labour for example - which is invariably present in modern global production, with companies always seeking out the lowest cost. Brooks writes: "Life is filled with tragic trade-offs. In many different venues, the suffering of the few is justified by those trying to deliver the greatest good for the greatest number.

"The story compels readers to ask if they are willing to live according to those contracts. Some are not. They walk away from prosperity, and they make some radical commitment... The rest of us live with the trade-offs... The people who stay in Omelas aren't bad; they just find it easier and easier to live with the misery they depend upon."

So here's a poser: What child is in the Singapore basement? To qualify, it would have to be something we are not proud to be associated with, but which exists nonetheless and can be rationalised in any number of ways, always for the greater public good. We don't need to be ashamed to ask this question because no society is perfect and all have their own demons. Different people will have different answers to the question but I can think of at least three candidates that a fair number might agree with.

The first would be low-wage workers left behind in the economic race that has brought the country to where it is today. In a nation with one of the highest per capita incomes in the world, it surprises many people that more than 200,000 residents earn less than $1,000 a month and struggle to cope with life here.

It's easy to rationalise their plight as a product of globalisation, and that a small open economy has to accept what the world is willing to pay for these workers. To be fair to this child in the basement, more people today are beginning to ask for more to be done to improve their lot. Programmes such as Workfare and the progressive wage system that the labour movement is championing have been introduced in response to these calls.

For some, another group would be political opponents of the ruling party and activists who have suffered as a result of their beliefs and actions, some of them severely so, during the uncompromising days of the 1960s to the 1980s.This is a diverse group, including those detained because of the alleged Marxist conspiracy of 1987 and later freed or who escaped, and assorted politicians who have felt the full brunt of the ruling party's power.

This isn't a column about the rights or wrongs of each of these cases.What I think most people would agree with is that they mainly occurred during a time in Singapore's history when the politics was rough in a way that would be out of place today.The issues they were associated with might no longer be relevant - too many years have passed - but for some, the shadow of that period lingers. Occasionally, they spring to life as in the controversy over the banning of the film, To Singapore With Love, and the running debate over which version of Singapore's political history is accurate.

The ghost of that child continues to haunt some.

A third group would be the large numbers of low-wage foreign workers and maids brought in to do jobs no one else wants to do. Their living and workplace conditions, the circumstances under which they are brought here, paying large fees to labour contractors, and their general alienation from the local population are issues most Singaporeans would rather not know about. Too many see and treat them as economic digits brought here to do a job and best kept out of trouble.

A child in the basement? Some would say they fit the bill perfectly. These examples show that the trade-offs that every society makes abound, balancing what they perceive to be for the greater good with the suffering of the few, but they are also not unchanging.

In all three examples I have cited, things are getting better. The income divide is being tackled, foreign workers' living conditions are being improved and Singapore's political culture is changing. Much of this change occurs at the individual level first - what pricks the conscience of Singaporeans, what they believe is right or wrong. These are inner battles fought deep inside our own basements.

You could say more Singaporeans are walking away from their Omelas, and the city changes as a result.

The Straits Times, 27th January 2015

There is this child who is kept locked in a basement in utter misery, deprived and tortured. The author does not say why this is so, or what the child has done to deserve this terrible imprisonment.Only that it is necessary for the city's continued success and contentment. Free him and everything that made the city such a wonderful place will disappear.

"They all know it is there, all the people of Omelas. Some of them have come to see it, others are content merely to know it is there. They all know that it has to be there. Some of them understand why, and some do not, but they all understand that their happiness, the beauty of their city, the tenderness of their friendships, the health of their children, the wisdom of their scholars, the skill of their makers, even the abundance of their harvest and the kindly weathers of their skies, depend wholly on this child's abominable misery."

Most accept this unwritten social contract that guarantees their happiness.But not everyone is happy with this state of affairs. There are those who cannot stand the injustice and leave the city.

"They leave Omelas, they walk ahead into the darkness, and they do not come back. The place they go towards is a place even less imaginable to most of us than the city of happiness. I cannot describe it at all. It is possible that it does not exist. But they seem to know where they are going, the ones who walk away from Omelas."

As you can see, it is a strange tale but even based on this very short summary, most of us instinctively understand what the story is about and can identify with the troubling issues this allegory raises.

Writing in The New York Times earlier this month, David Brooks offered various interpretations of the story. One is that it's about exploitation - of cheap labour for example - which is invariably present in modern global production, with companies always seeking out the lowest cost. Brooks writes: "Life is filled with tragic trade-offs. In many different venues, the suffering of the few is justified by those trying to deliver the greatest good for the greatest number.

"The story compels readers to ask if they are willing to live according to those contracts. Some are not. They walk away from prosperity, and they make some radical commitment... The rest of us live with the trade-offs... The people who stay in Omelas aren't bad; they just find it easier and easier to live with the misery they depend upon."

So here's a poser: What child is in the Singapore basement? To qualify, it would have to be something we are not proud to be associated with, but which exists nonetheless and can be rationalised in any number of ways, always for the greater public good. We don't need to be ashamed to ask this question because no society is perfect and all have their own demons. Different people will have different answers to the question but I can think of at least three candidates that a fair number might agree with.

The first would be low-wage workers left behind in the economic race that has brought the country to where it is today. In a nation with one of the highest per capita incomes in the world, it surprises many people that more than 200,000 residents earn less than $1,000 a month and struggle to cope with life here.

It's easy to rationalise their plight as a product of globalisation, and that a small open economy has to accept what the world is willing to pay for these workers. To be fair to this child in the basement, more people today are beginning to ask for more to be done to improve their lot. Programmes such as Workfare and the progressive wage system that the labour movement is championing have been introduced in response to these calls.

For some, another group would be political opponents of the ruling party and activists who have suffered as a result of their beliefs and actions, some of them severely so, during the uncompromising days of the 1960s to the 1980s.This is a diverse group, including those detained because of the alleged Marxist conspiracy of 1987 and later freed or who escaped, and assorted politicians who have felt the full brunt of the ruling party's power.

This isn't a column about the rights or wrongs of each of these cases.What I think most people would agree with is that they mainly occurred during a time in Singapore's history when the politics was rough in a way that would be out of place today.The issues they were associated with might no longer be relevant - too many years have passed - but for some, the shadow of that period lingers. Occasionally, they spring to life as in the controversy over the banning of the film, To Singapore With Love, and the running debate over which version of Singapore's political history is accurate.

The ghost of that child continues to haunt some.

A third group would be the large numbers of low-wage foreign workers and maids brought in to do jobs no one else wants to do. Their living and workplace conditions, the circumstances under which they are brought here, paying large fees to labour contractors, and their general alienation from the local population are issues most Singaporeans would rather not know about. Too many see and treat them as economic digits brought here to do a job and best kept out of trouble.

A child in the basement? Some would say they fit the bill perfectly. These examples show that the trade-offs that every society makes abound, balancing what they perceive to be for the greater good with the suffering of the few, but they are also not unchanging.

In all three examples I have cited, things are getting better. The income divide is being tackled, foreign workers' living conditions are being improved and Singapore's political culture is changing. Much of this change occurs at the individual level first - what pricks the conscience of Singaporeans, what they believe is right or wrong. These are inner battles fought deep inside our own basements.

You could say more Singaporeans are walking away from their Omelas, and the city changes as a result.

The Straits Times, 27th January 2015

Why The Swiss Unpegged The Franc

IN THE world of central banking, slow and predictable decisions are the aim. So on January 15th, when the Swiss National Bank (SNB) suddenly announced that it would no longer hold the Swiss franc at a fixed exchange rate with the euro, there was panic. The franc soared. On Wednesday one euro was worth 1.2 Swiss francs; at one point on Thursday its value had fallen to just 0.85 francs. A number of hedge funds across the world made big losses. The Swiss stockmarket collapsed. Why did the SNB provoke such chaos?

The SNB introduced the exchange-rate peg in 2011, while financial markets around the world were in turmoil. Investors consider the Swiss franc as a “safe haven” asset, along with American government bonds: buy them and you know your money will not be at risk. Investors like the franc because they think the Swiss government is a safe pair of hands: it runs a balanced budget, for instance. But as investors flocked to the franc, they dramatically pushed up its value. An expensive franc hurts Switzerland because the economy is heavily reliant on selling things abroad: exports of goods and services are worth over 70% of GDP. To bring down the franc’s value, the SNB created new francs and used them to buy euros. Increasing the supply of francs relative to euros on foreign-exchange markets caused the franc’s value to fall (thereby ensuring a euro was worth 1.2 francs). Thanks to this policy, by 2014 the SNB had amassed about $480 billion-worth of foreign currency, a sum equal to about 70% of Swiss GDP.

The SNB suddenly dropped the cap last week for several reasons. First, many Swiss are angry that the SNB has built up such large foreign-exchange reserves. Printing all those francs, they say, will eventually lead to hyperinflation. Those fears are probably unfounded: Swiss inflation is too low, not too high. But it is a hot political issue. In November there was a referendum which, had it passed, would have made it difficult for the SNB to increase its reserves. Second, the SNB risked irritating its critics even more, thanks to something that is happening this Thursday: many expect the European Central Bank to introduce “quantitative easing”. This entails the creation of money to buy the government debt of euro-zone countries. That will push down the value of the euro, which might have required the SNB to print lots more francs to maintain the cap. But there is also a third reason behind the SNB’s decision. During 2014 the euro depreciated against other major currencies. As a result, the franc (being pegged to the euro) has depreciated too: in 2014 it lost about 12% of its value against the dollar and 10% against the rupee (though it appreciated against both currencies following the SNB's decision). A cheaper franc boosts exports to America and India, which together make up about 20% of Swiss exports. If the Swiss franc is not so overvalued, the SNB argues, then it has no reason to continue trying to weaken it.

The big question now is how much the removal of the cap will hurt the Swiss economy. The stockmarket fell because Swiss companies will now find it more difficult to sell their wares to European customers (high-rolling Europeans are already complaining about the price of this year’s skiing holidays). UBS, a bank, downgraded its forecast for Swiss growth in 2015 from 1.8% to 0.5%. Switzerland will probably remain in deflation. But the SNB should not be lambasted for removing the cap. Rather, it should be criticised for adopting it in the first place. When central banks try to manipulate exchange rates, it almost always ends in tears.

The Economist, January 18th 2015

The SNB introduced the exchange-rate peg in 2011, while financial markets around the world were in turmoil. Investors consider the Swiss franc as a “safe haven” asset, along with American government bonds: buy them and you know your money will not be at risk. Investors like the franc because they think the Swiss government is a safe pair of hands: it runs a balanced budget, for instance. But as investors flocked to the franc, they dramatically pushed up its value. An expensive franc hurts Switzerland because the economy is heavily reliant on selling things abroad: exports of goods and services are worth over 70% of GDP. To bring down the franc’s value, the SNB created new francs and used them to buy euros. Increasing the supply of francs relative to euros on foreign-exchange markets caused the franc’s value to fall (thereby ensuring a euro was worth 1.2 francs). Thanks to this policy, by 2014 the SNB had amassed about $480 billion-worth of foreign currency, a sum equal to about 70% of Swiss GDP.

The SNB suddenly dropped the cap last week for several reasons. First, many Swiss are angry that the SNB has built up such large foreign-exchange reserves. Printing all those francs, they say, will eventually lead to hyperinflation. Those fears are probably unfounded: Swiss inflation is too low, not too high. But it is a hot political issue. In November there was a referendum which, had it passed, would have made it difficult for the SNB to increase its reserves. Second, the SNB risked irritating its critics even more, thanks to something that is happening this Thursday: many expect the European Central Bank to introduce “quantitative easing”. This entails the creation of money to buy the government debt of euro-zone countries. That will push down the value of the euro, which might have required the SNB to print lots more francs to maintain the cap. But there is also a third reason behind the SNB’s decision. During 2014 the euro depreciated against other major currencies. As a result, the franc (being pegged to the euro) has depreciated too: in 2014 it lost about 12% of its value against the dollar and 10% against the rupee (though it appreciated against both currencies following the SNB's decision). A cheaper franc boosts exports to America and India, which together make up about 20% of Swiss exports. If the Swiss franc is not so overvalued, the SNB argues, then it has no reason to continue trying to weaken it.

The big question now is how much the removal of the cap will hurt the Swiss economy. The stockmarket fell because Swiss companies will now find it more difficult to sell their wares to European customers (high-rolling Europeans are already complaining about the price of this year’s skiing holidays). UBS, a bank, downgraded its forecast for Swiss growth in 2015 from 1.8% to 0.5%. Switzerland will probably remain in deflation. But the SNB should not be lambasted for removing the cap. Rather, it should be criticised for adopting it in the first place. When central banks try to manipulate exchange rates, it almost always ends in tears.

The Economist, January 18th 2015

Swiss bank’s currency U-turn hurts watchmakers, skiers and traders

Central bank’s abandonment of Swiss franc-euro cap described as a ‘tsunami of pain’ for exporters and tourism industry.

Watch makers, ski resorts and currency traders were facing big losses on Thursday when the Swiss central bank stunned the financial markets by abandoning its currency peg against the euro.

Swiss manufacturers faced what one business leader described as a “tsunami” of financial pain as the franc responded to the shock announcement, jumping by an initial 30% against the euro. Movements of around 2% are usually considered big in the foreign exchange markets.

The move wiped 9% off the value of the Swiss stock market – its biggest one-day fall in more than 25 years. One trader described the market reaction as “complete carnage”.The Swiss action is the latest event to unsettle markets since the turn of the year and came amid growing concern about the health of the global economy and warnings from the International Monetary Fund that the recovery since the recession of 2008-09 remained weak.

Speaking iIn the US, IMF director general Christine Lagarde said global growth was “still too low, too brittle and too lopsided”. There was a risk, she added, of the eurozone and Japan getting stuck in a world of low growth and low inflation for a prolonged period.

Strong signs that the European Central Bank (ECB) will announce a large-scale programme of quantitative easing (QE) – electronic money printing – to lift the eurozone out of deflation was seen by currency traders as the main reason for the Swiss National Bank (SNB) ditching its three-year campaign to stop the franc damaging Swiss exports by becoming too strong against the euro.But with rich Russians looking for a safe haven during the recent rouble crisis, hot money has also been flowing into Switzerland in recent weeks, adding to the SNB’s difficulties in holding down the franc.

Swiss central bank chairman Thomas Jordan said that after more than three years in force the policy was no longer needed. The swiss franc/euro exchange rate did come back to a gain of 15% on the day. But Swiss businesses flatly rejected Jordan’s explanation. Banks, manufacturers and the tourist industry lined up to condemn the bank for its decision, which will make Swiss holidays and goods far more expensive.

Manufacturers in Switzerland’s northern belt are likely to feel the impact first as their exports to Germany and other eurozone countries become far pricier.Nick Hayek, the chief executive of the Swatch watch group – which owns brands such as Omega, Longines, Tissot and Calvin Klein watches and jewellery – said: “Words fail me …today’s SNB action is a tsunami; for the export industry and for tourism, and finally for the entire country.”

Swiss watchmakers are already grappling with weak demand in Asia, and are very exposed to moves in the Swiss franc exchange rate because they export almost all they produce. Shares in Swatch Group tumbled by 15%, while Richemont, which owns luxury names including Cartier, Montblanc and the fashion label Chloé, was down 14%.

The London spread-betting business IG Group said bets on the Swiss franc could cost it as much as £30m. Julien Manceaux, analyst at ING Financial Markets, said the central bank’s cut in its interest rate to minus 0.75% “ensures the appetite for the franc as a safe haven will remain limited, avoiding a negative shock for the Swiss economy”. “This should work at least in the near term. Whether, this will still be the case after the ECB’s meeting on 22nd January and a likely QE announcement remains to be seen.”

The tourism industry will be hard hit as the cost of holidays soars, with a sharp decline expected in bookings to Alpine ski resorts at a peak time for the industry.The euro declined to 0.80 francs before recovering slightly to stand at 1.03 francs. The franc also gained 25% against the dollar to trade at 0.89 francs per dollar.

One investment firm was forced to admit that the sudden shift in the Swiss franc had cost it as much as £30m. The spike rise in the value of the Swiss franc came in early trading after the Swiss National Bank’s chairman Thomas Jordan said in a statement that the cap, introduced in September 2011, “protected the Swiss economy from serious harm” but was no longer justified.

The bank said the measure, which in effectively pegged the Swiss franc to the euro, meant the franc has tracked the euro during a period when it has dropped sharply against the US dollar. Switzerland is seen by investors as a safe haven by wealthy investors and corporations fearful of destabilising developments in Russia and the Middle East. Investors have also flocked to Switzerland to escape ultra-low interest rates in the eurozone.

Pressure has intensified on the franc since the ECB hinted that it would begin flooding the eurozone with cheap credit under a programme of quantitative easing (QE), a move expected to reduce long-term interest rates further and devalue the euro against other currencies.

An advocate general’s ruling this week, likely to be accepted by the European Court of Justice, said the ECB was free to press ahead with bond buying without legal challenge. This intensified speculation that QE was imminent, forcing the SNB’s hand.

The growing US economy, and the likelihood of an increase in interest rates this year, has also pushed the dollar higher, exacerbating the widening gap between the dollar and euro. At 11.00 the euro was down a cent against the dollar at $1.68 while the pound was up a cent at $1.52. The Swiss stock market collapsed 10%, or almost 1,000 points, to hit 8,205. With the likelihood of money flooding out of the eurozone in search of higher interest rates, the SNB’s cut in its deposit rate by 0.5 percentage points to -0.75 is intended to be a deterrent to investors thinking of Zurich as an alternative home for their investment savings.

The Guardian, 15th January 2015

Watch makers, ski resorts and currency traders were facing big losses on Thursday when the Swiss central bank stunned the financial markets by abandoning its currency peg against the euro.

Swiss manufacturers faced what one business leader described as a “tsunami” of financial pain as the franc responded to the shock announcement, jumping by an initial 30% against the euro. Movements of around 2% are usually considered big in the foreign exchange markets.

The move wiped 9% off the value of the Swiss stock market – its biggest one-day fall in more than 25 years. One trader described the market reaction as “complete carnage”.The Swiss action is the latest event to unsettle markets since the turn of the year and came amid growing concern about the health of the global economy and warnings from the International Monetary Fund that the recovery since the recession of 2008-09 remained weak.

Speaking iIn the US, IMF director general Christine Lagarde said global growth was “still too low, too brittle and too lopsided”. There was a risk, she added, of the eurozone and Japan getting stuck in a world of low growth and low inflation for a prolonged period.

Strong signs that the European Central Bank (ECB) will announce a large-scale programme of quantitative easing (QE) – electronic money printing – to lift the eurozone out of deflation was seen by currency traders as the main reason for the Swiss National Bank (SNB) ditching its three-year campaign to stop the franc damaging Swiss exports by becoming too strong against the euro.But with rich Russians looking for a safe haven during the recent rouble crisis, hot money has also been flowing into Switzerland in recent weeks, adding to the SNB’s difficulties in holding down the franc.

Swiss central bank chairman Thomas Jordan said that after more than three years in force the policy was no longer needed. The swiss franc/euro exchange rate did come back to a gain of 15% on the day. But Swiss businesses flatly rejected Jordan’s explanation. Banks, manufacturers and the tourist industry lined up to condemn the bank for its decision, which will make Swiss holidays and goods far more expensive.

Manufacturers in Switzerland’s northern belt are likely to feel the impact first as their exports to Germany and other eurozone countries become far pricier.Nick Hayek, the chief executive of the Swatch watch group – which owns brands such as Omega, Longines, Tissot and Calvin Klein watches and jewellery – said: “Words fail me …today’s SNB action is a tsunami; for the export industry and for tourism, and finally for the entire country.”

Swiss watchmakers are already grappling with weak demand in Asia, and are very exposed to moves in the Swiss franc exchange rate because they export almost all they produce. Shares in Swatch Group tumbled by 15%, while Richemont, which owns luxury names including Cartier, Montblanc and the fashion label Chloé, was down 14%.

The London spread-betting business IG Group said bets on the Swiss franc could cost it as much as £30m. Julien Manceaux, analyst at ING Financial Markets, said the central bank’s cut in its interest rate to minus 0.75% “ensures the appetite for the franc as a safe haven will remain limited, avoiding a negative shock for the Swiss economy”. “This should work at least in the near term. Whether, this will still be the case after the ECB’s meeting on 22nd January and a likely QE announcement remains to be seen.”

The tourism industry will be hard hit as the cost of holidays soars, with a sharp decline expected in bookings to Alpine ski resorts at a peak time for the industry.The euro declined to 0.80 francs before recovering slightly to stand at 1.03 francs. The franc also gained 25% against the dollar to trade at 0.89 francs per dollar.

One investment firm was forced to admit that the sudden shift in the Swiss franc had cost it as much as £30m. The spike rise in the value of the Swiss franc came in early trading after the Swiss National Bank’s chairman Thomas Jordan said in a statement that the cap, introduced in September 2011, “protected the Swiss economy from serious harm” but was no longer justified.

The bank said the measure, which in effectively pegged the Swiss franc to the euro, meant the franc has tracked the euro during a period when it has dropped sharply against the US dollar. Switzerland is seen by investors as a safe haven by wealthy investors and corporations fearful of destabilising developments in Russia and the Middle East. Investors have also flocked to Switzerland to escape ultra-low interest rates in the eurozone.

Pressure has intensified on the franc since the ECB hinted that it would begin flooding the eurozone with cheap credit under a programme of quantitative easing (QE), a move expected to reduce long-term interest rates further and devalue the euro against other currencies.

An advocate general’s ruling this week, likely to be accepted by the European Court of Justice, said the ECB was free to press ahead with bond buying without legal challenge. This intensified speculation that QE was imminent, forcing the SNB’s hand.

The growing US economy, and the likelihood of an increase in interest rates this year, has also pushed the dollar higher, exacerbating the widening gap between the dollar and euro. At 11.00 the euro was down a cent against the dollar at $1.68 while the pound was up a cent at $1.52. The Swiss stock market collapsed 10%, or almost 1,000 points, to hit 8,205. With the likelihood of money flooding out of the eurozone in search of higher interest rates, the SNB’s cut in its deposit rate by 0.5 percentage points to -0.75 is intended to be a deterrent to investors thinking of Zurich as an alternative home for their investment savings.

The Guardian, 15th January 2015

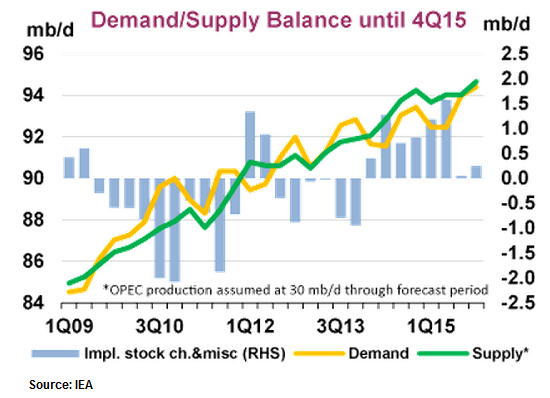

Why are oil prices falling - explained in 60 seconds

Get Used to Cheap Oil. Why Lower Prices May Stick Around

Oil’s plunge is one of the biggest factors reshaping the global economy. How long can it last? Here are two fundamental reasons oil prices could stay low for a while.

1. Excess capacity

Prices are determined by the size of the gap between demand and supply. Both sides of the ledger have been dramatically adjusted in the last several months to widen that gap, leading to the price plunge. Saudi Arabia in particular moved to recapture market share lost to the U.S. by keeping the crude spigots open regardless of price. And as the global economic outlook dimmed, demand has fallen, with sharp revisions in expected growth in crude oil consumption.

The International Energy Agency predicts a much tighter balance between supply and demand late in the year as the more expensive production is squeezed out of the market:

1. Excess capacity

Prices are determined by the size of the gap between demand and supply. Both sides of the ledger have been dramatically adjusted in the last several months to widen that gap, leading to the price plunge. Saudi Arabia in particular moved to recapture market share lost to the U.S. by keeping the crude spigots open regardless of price. And as the global economic outlook dimmed, demand has fallen, with sharp revisions in expected growth in crude oil consumption.

The International Energy Agency predicts a much tighter balance between supply and demand late in the year as the more expensive production is squeezed out of the market:

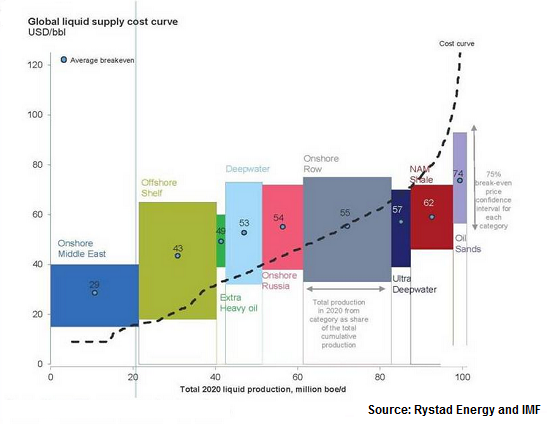

Producers on the top end of the cost curve are more at risk, with oil sands leading the pack.

While firms may shut down production, traders know it could come back online in a relatively short period of time. That’s one reason prices remained low for 15 years after the 1985-1986 oil price collapse, an episode that some economists see as a parallel to today’s price plunge.

And the gap between global demand and total production capacity is much larger than many realize. The IEA and the U.S. Energy Information Administration only count barrels that can come online within a few weeks in their excess-capacity calculations.

Leonardo Maugeri, an associate professor at Harvard University’s Belfer Center for Science and International Affairs and who predicted the current collapse in prices back in 2012, estimates world oil production capacity is about 101 million barrels a day. That’s nearly 10% more than expected demand next year.

Mr. Maugeri says U.S. shale and tight oil production is more resilient than many expected because of lower break-even costs and higher productivity levels. Service fees are also falling at the same time, as hedging still offers a cushion to shale producers until mid-2015, he said. That resilience may force Saudi Arabia to keep up its price war well into the year before the strategy wrings out some of the oversupply. Elsewhere in the world, Mr. Maugeri said oil producers will likely slash exploration, but not development spending, which means new capacity will still come online.

2. Stalled Demand

Cheap fuel should, theoretically, drive up consumption as consumers spend their windfall and juice economic growth. That’s a major reason the International Monetary Fund revised up its projection for U.S. growth this year.

But tumbling oil prices are also signaling global economic weakness, and there’s no certainty demand will rebound anytime in the near future. In fact, the IMF cut prospects for the global economy and said the shot in the arm for tumbling crude costs wouldn’t be enough to pull the world out of a deepening long-term rut.

Two of the world’s biggest economies–the eurozone and Japan—are struggling to avoid re-entering recessions and are expected to remain stuck in stagnant growth for years to come. Falling oil prices appear to be feeding lower inflation expectations. Consumers and businesses may cut back on spending if they expect prices to fall further. And outright deflation makes government debt problems worse, pushing up borrowing costs even while growth prospects dim.

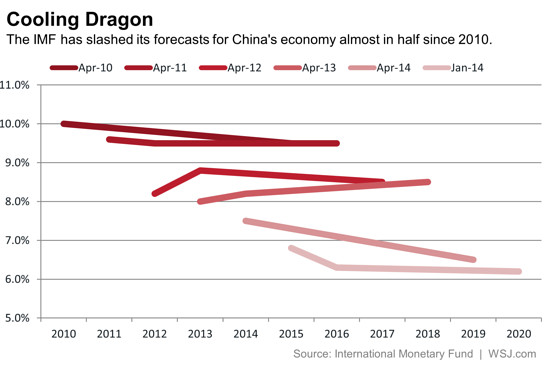

Also, one of the biggest drivers of oil’s rise–China–is slowing much faster than many expected. Just as the world’s No. 2 economy pushed prices toward $150 a barrel before the financial crisis with a growth rate above 14% in 2007, cuts in the country’s outlook have accelerated oil’s price decline. The IMF late Monday slashed its growth expectations again, putting the country’s expansion at the lowest rate in 24 years.

And the gap between global demand and total production capacity is much larger than many realize. The IEA and the U.S. Energy Information Administration only count barrels that can come online within a few weeks in their excess-capacity calculations.

Leonardo Maugeri, an associate professor at Harvard University’s Belfer Center for Science and International Affairs and who predicted the current collapse in prices back in 2012, estimates world oil production capacity is about 101 million barrels a day. That’s nearly 10% more than expected demand next year.

Mr. Maugeri says U.S. shale and tight oil production is more resilient than many expected because of lower break-even costs and higher productivity levels. Service fees are also falling at the same time, as hedging still offers a cushion to shale producers until mid-2015, he said. That resilience may force Saudi Arabia to keep up its price war well into the year before the strategy wrings out some of the oversupply. Elsewhere in the world, Mr. Maugeri said oil producers will likely slash exploration, but not development spending, which means new capacity will still come online.

2. Stalled Demand

Cheap fuel should, theoretically, drive up consumption as consumers spend their windfall and juice economic growth. That’s a major reason the International Monetary Fund revised up its projection for U.S. growth this year.

But tumbling oil prices are also signaling global economic weakness, and there’s no certainty demand will rebound anytime in the near future. In fact, the IMF cut prospects for the global economy and said the shot in the arm for tumbling crude costs wouldn’t be enough to pull the world out of a deepening long-term rut.

Two of the world’s biggest economies–the eurozone and Japan—are struggling to avoid re-entering recessions and are expected to remain stuck in stagnant growth for years to come. Falling oil prices appear to be feeding lower inflation expectations. Consumers and businesses may cut back on spending if they expect prices to fall further. And outright deflation makes government debt problems worse, pushing up borrowing costs even while growth prospects dim.

Also, one of the biggest drivers of oil’s rise–China–is slowing much faster than many expected. Just as the world’s No. 2 economy pushed prices toward $150 a barrel before the financial crisis with a growth rate above 14% in 2007, cuts in the country’s outlook have accelerated oil’s price decline. The IMF late Monday slashed its growth expectations again, putting the country’s expansion at the lowest rate in 24 years.

The Wall Street Journal. 21/01/2015

Students' Reflections

Economics is a subject totally new to us. Based on our understanding of the word 'economics' , we thought that it is a subject that teaches us about the financial system of different countries as well as how money is circulated around the world. We think because of its relevance to our daily lives and also the world ,it brings us closer to the outside world. We initially thought that Economics will be a really dry subject because we heard that its all about finance and graphs. However up till now, all that have been taught are pretty interesting; like how demand and supply is so close to us , how resources are allocated and how money is spent to maximise satisfaction. Everything makes sense to us and was not as hard to understand as we thought it would be. Through economics , we hope to learn more about the different aspects of an economy and find out how economics can affect different individuals in a country . We find that economics so far is really fun and interesting as it brings us a different perspective of how people see the economy. We are really excited for future lessons to come.

Shania Chua, 1511

Kares Yap, 1511

Zheng Zhifang, 1511

Shania Chua, 1511

Kares Yap, 1511

Zheng Zhifang, 1511

Our first impression of economics was that it is the study of how the world economy functions and its complexities. We felt very uncertain about how do go about studying economics as it is a very new and fresh subject to us. Feelings of apprehension were also very apparent to us when we had our first ever Economics Lecture. However, after these past few weeks of exposure to the subject, we have gained a better understanding of the subject. We have learned that Economics is more than numbers and figures, it also involves many concepts which are applicable in our everyday lives. The study of economics has allowed us to develop a more critical approach towards the complexities and dimensions around us. We find ourselves analysing articles with more depth and thinking about the possible economic reasoning behind them . Economics has now piqued our interest as it reflects the reality of our economy and how economic decisions affect stakeholders like us. Overall, we have grown to develop an interest towards the subject as a whole, and we are certainly looking forward to learning more about this subject!

Teo Xi Hui 1506

Lim Jia Ying 1506

Teo Xi Hui 1506

Lim Jia Ying 1506